What did your accounting tell you today?

Sometimes business owners are guilty of over examining accounting records, looking for the answer. Developing a list of key performance indicators (KPI’s) is better, but can still be overdone. Usually five is enough. The importance of measuring to improve gets confusing when you don’t know what you should be measuring.

Instead of trying to answer every possible question or problem in your organization, try breaking this down into a few straightforward questions, with straightforward answers. This evening I went to a Mexican restaurant. Facing me as I entered the building was a whiteboard listing the specials tonight.

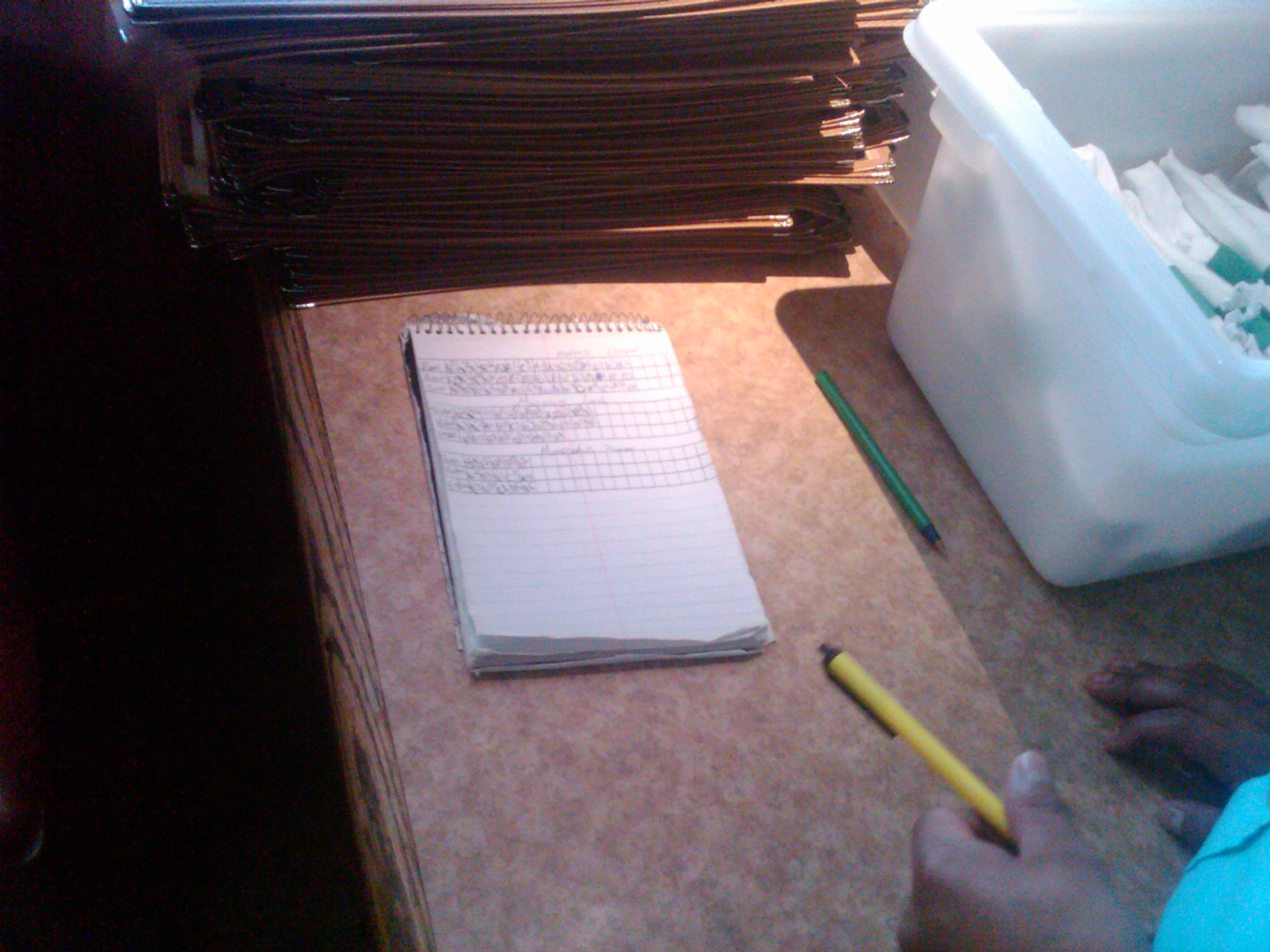

At first it didn’t strike me as that interesting. After all, what Mexican restaurant doesn’t have a list of specials? What I did find interesting however was this booklet that was used by the waiters to track how many of each special that was sold. A simple problem (which specials sells the best on Wednesday night), answered with a simple tracking system (spiral bound notebook).

Once I worked with a child care center that had a problem with teachers showing up for their shift 5-15 minutes late. It was a big problem because the state mandated a specific child to teacher ratio. If kids showed up early, or even on time and the teachers were late, fines were imposed. I recommended tracking teacher tardiness on a simple spreadsheet and then posting the weekly results above the time clock for everyone to see. Within two weeks everyone was showing up on time. Nobody wanted to be the offender.

Don’t get too bogged down with esoteric measurement systems. Consider some easily solvable problems and conquer those first.

Posted in: Blog

Leave a Comment (0) →